PKP: Take out the alcohol from a drink. Still get a buzz… no hang over - but how?

Alcohol sales are declining…

And cannabis infused versions of these drinks are coming in.

THC is the active compound in cannabis that gives the high/buzz.

THC offers a controlled, alcohol-like effect with fewer drawbacks - no hangovers, less calories...

... a healthier, modern alternative to alcoholic drinks.

Our Investment for the THC drinks sector is the $20M capped Peak Processing Ltd (ASX: PKP).

PKP has developed a product that allows major drinks brands to replace the alcohol in their most popular drinks with… THC.

PKP is a “picks and shovels” style investment for the cannabis drinks sector.

Existing big drinks companies can approach PKP to add THC to any kind of drink - think cannabis infused iced tea, cola, beer, vodka, seltzers - or any other flavour.

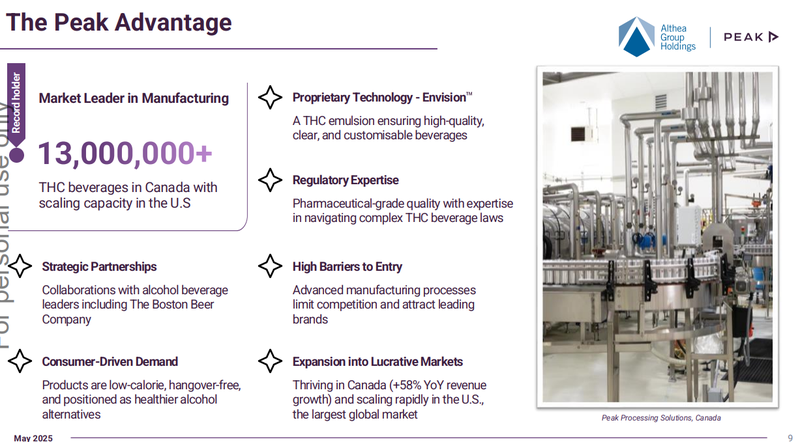

PKP is a well established, revenue generating company.

The company is a market leader in Canada, manufacturing ~33% of all cans produced in the THC drinks market and last year launched into the US - opening a processing facility in Florida.

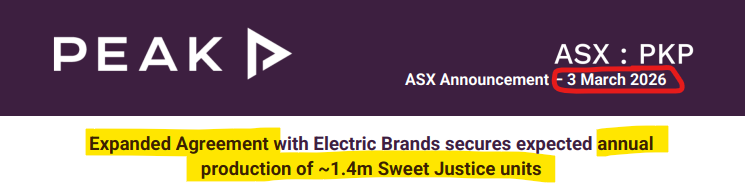

Today PKP just expanded one of its largest manufacturing deals.

(source)

PKP signed an expansion deal with Electric Brands to continue manufacturing the “Sweet Justice” cannabis drink portfolio.

Sweet Justice is one of PKP’s longest-running and largest manufacturing deals - totalling ~1.4M units per annum.

It’s also one of the top selling brands in Canada.

(PKP has been manufacturing for Sweet Justice since 2020)

(source - PKP manufactures these^)

Today’s new agreement adds to the string of newsflow from PKP over the last two months.

When you add up the:

- Organigram/Collective deal in December (approx 1.5 mill cans),

- A 250% expansion to the St Peters (Cookies and Green Monkey) manufacturing agreement. (Approx ~700,000 cans) (Source)

- and now today's expanded deal at over 1.4 million cans,

PKP has secured close to 3 million cans, a big chunk of PKP’s current production capacity.

Last month PKP raised $2.72M at 1.7c a share, so it looks well funded to execute on its strategy in 2026. It was excellent to see the board and key management participating in this placement.

We think today’s announcement is a strong signal that PKP is protecting its market leading position in Canada for brands looking for a manufacturing supplier.

Right now, PKP produces for ~70% of all brands operating in the Canadian market.

And as we said above, in terms of manufacturing, PKP has ~33% of market shares across the entire Canadian THC-infused beverage market. (source)

(hence the “picks and shovels” analogy we like to use)

(source)

A big part of the reason we Invested in PKP was because the Canadian business is already generating revenues.

And with overall market growth in the THC drinks space, PKP could grow in size and eventually become highly profitable.

More importantly, though, the successful Canadian business could be used as a springboard to a larger market rollout in the US… (and eventually maybe in other parts of the world)

Canada is a highly regulated market and has reached US$580M in value as of 2023 (source).

Which makes it the perfect place for big conglomerates to build new products from scratch and have them ready for global launch - when regulations change in other jurisdictions.

PKP already has the #1 THC drink manufacturing business in Canada (where THC drinks are legal and sold in regulated dispensaries).

IF the company can do it in one of the most regulated markets in the world - then surely it could take that business model and apply it to other markets as regulation changes.

So it was good to see today’s announcement mention PKP was “in advanced negotiations with several parties” to scale its North American presence.

(source)

What is PKP up to in the US right now?

Earlier in the year, PKP opened up a new manufacturing facility in Florida to target the US market, where THC drinks are taking off. (Source)

In the coming years, the USA is estimated to be a 15x bigger market (~$30BN by 2028) than Canada ($1.8BN by 2028).

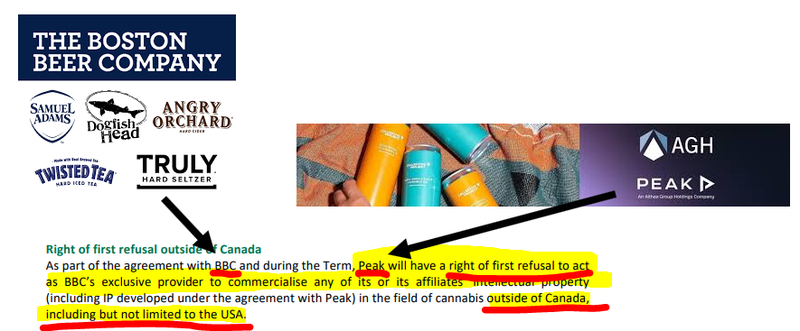

PKP is already working with some of the big alcohol companies - like $3.4BN Boston Beer Co and $190BN British American Tobacco.

Boston Beer company has over US$2.1BN revenue per year and is best known for

- Samuel Adams (craft beer)

- Truly Hard Seltzer

- Twisted Tea (alcoholic tea)

- Angry Orchard (hard cider)

- Dogfish Head (craft beer)

- Hard Mountain Dew (in partnership)

The big one for them is “Twisted Tea” which sold 33 million cans in 2024 and is the best selling “hard tea” with more than 80% market share in the USA. (Source)

PKP partners with Boston Beer Co to make a non-alcoholic, THC-infused version of Twisted Tea for sale in Canada (branded as Teapot).

So far, Boston Beer Company hasn't launched a THC drink in the US…

The big kicker with PKP’s Boston Beer Company partnership is PKP’s right of first refusal on contract manufacturing for them in the US. (source)

(Source)

So IF Boston Beer Company decides to launch any THC drink into the US... it could be a game changer for PKP.

PKP’s THC-infusion can be applied to ANY drink, so any big alcohol company can use PKP to make a non-alcoholic, THC-infused version of any of their popular drink brands.

We think PKP’s market leading position in the highly regulated Canadian market means it could position itself as the most trusted partner for these major alcohol companies to work with.

All we need now is for the current “cowboy” USA THC drinks industries regulations to be changed and open the door for the bigger companies to launch drinks without major friction points in the industry.

Which looks like it could happen in the medium term - we covered the status of regulation in the US in our last note in detail.

Check that out here: The latest on the THC drinks industry in the US

Why we Invested in PKP

THC-infused drinks are one of the fastest growing consumer industries in the USA - becoming more popular as a replacement for alcoholic drinks.

THC (tetrahydrocannabinol) is the main psychoactive compound found in the cannabis plant -

in other words it's the substance in marijuana that gets you high.

PKP’s manufacturing division (Peak Processing Solutions) holds a ~33% share of the Canadian THC-infused beverage market, representing around 28% of all national brands.

AND last year PKP opened a manufacturing facility in Florida (USA), looking to replicate the success and growth shown from the Canadian market.

(Source)

Our Investment in PKP comes off the back of a macro background of alcohol sales reducing, with the same article above stating a 23 year low in beer consumption (despite a 23% population increase) with younger generations drinking less alcohol per capita than baby boomers.

So there is a gap in the market that THC beverages in particular are looking to fill.

The 11 reasons we invested in PKP

We Invested in PKP back in July last year at 2.5c per share.

For those who haven’t read it yet, check out our most recent note: PKP: New name. New (big) customer. New alternative to drinking alcohol - cannabis beverages.

Here is a quick overview of the 11 key reasons why we are Invested in PKP. These are all in our most recent coverage linked just above.

11 Reasons why we Invested in PKP

We Invested in PKP back in July last year, check out our Investment memo for why we made our Investment including the macro theme that we are expecting to play out in coming years..

Here are the 11 reasons that we have for making our PKP Investment:

- Consumer drinking habits are changing, THC drinks to replace alcohol?

- PKP is the biggest manufacturer of THC beverages in Canada

- Canadian business has capacity to grow even further

- PKP has just entered the US market - the fastest growing market for THC Beverages

- PKP is adopting a Coca-Cola style distribution model in the US

- PKP already has deals with major companies like Boston Beer Co.

- PKP also has its own brands… one could go “viral”

- PKP has just gone through a restructure

- Big Alcohol has invested in THC drinks - will they do it again?

- PKP can make, design and produce THC versions of ANY existing and popular drink

- THC drinks could have a “popularity” wave

Ultimately we are hoping the reasons above contribute toward PKP achieving our Big Bet which is as follows:

Our PKP Big Bet:

“PKP re-rates to a $200M+ market cap on the back of strong THC Beverage sales growth in North America”

NOTE: our “Big Bet” is what we HOPE the ultimate success scenario looks like for this particular Investment over the long term (3+ years). There is no guarantee that our Big Bet will ever come true. There is a lot of work to be done, many risks involved, including financing risk, regulatory risk, and market adoption risk - just some of which we list in our PKP Investment Memo.

Success will require a significant amount of luck and good management. Past performance is not an indicator of future performance.

Next, we want to see PKP:

- Increase capacity utilisation at its Canadian facility.

- Achieve profitability organisation-wide.

- Clearly define its US growth strategy given the recent regulatory changes.

What are the risks?

In the short-medium term the two key risks we see for PKP is “regulatory risk” and “financing risk”.

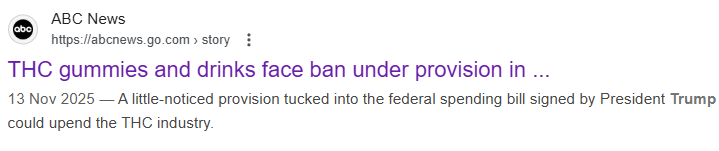

A big reason for our Investment is for the US expansion - there is always a risk that the grey areas in the 2018 Farm Bill, which permit hemp-derived THC are closed.

We did notice recently that Donald Trump signed a bill that would close the hemp-derived THC loophole to produce THC drinks - it’s not very clear how that impacts PKP at the moment.

BUT we think that in the short-term this could impact PKP’s US operations - and temper some of the market expectations that got priced into the PKP share price:

(source)

Regulatory Risk

Canada: The THC beverage market is tightly regulated. Any change in Canada’s regulatory environment could disrupt PKP’s ability to produce, sell, or distribute products.

United States: The market operates in a legal grey area under the 2018 Farm Bill, which permits hemp-derived THC (under 0.3% Delta-9 THC). However:

- Several states are cracking down (e.g., Texas is attempting bans).

- Regulatory uncertainty may limit national expansion, with state-by-state laws varying.

- A potential federal reclassification of cannabinoids could change market dynamics overnight.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

At the end of the December quarter (31 Dec 2025) PKP had ~$1.1M in debt outstanding and ~$685k cash. (source)

Since then PKP has gone onto raise $2.7M at 1.7c per share. (source),

It’s possible PKP needs to raise cash at some point in the future to shore up the company’s balance sheet and/or pursue accelerated growth.

PKP does generate revenues but the quarterly running costs for the company can be >$5M - in the December quarter so there is always a chance the company has short term working capital requirements that mean the company needs to raise cash.

Financing Risk

PKP is still in early commercialisation in the US and may need additional capital to expand into new states or marketing spend to build its brands.

In the absence of profitability, PKP may dilute shareholders through capital raises or struggle to fund growth internally.

Source: “What could go wrong” - PKP Investment Memo - 11 July 2025

Other risks

Like any small cap company operating in an emerging and highly regulated industry, PKP carries significant risk, here we aim to identify a few more risks.

PKP’s revenue model is heavily reliant on a small number of major contract manufacturing deals (such as the Sweet Justice expansion and the Boston Beer Co. partnership). If one of these key clients decides to move manufacturing in-house, switches to a competitor, or if their product sales decline significantly, PKP’s revenues and capacity utilisation would take a direct and material hit.

The THC beverage market is highly competitive and rapidly evolving. While PKP currently holds a strong market share in Canada (~33%), there are low barriers to entry for new contract manufacturers or existing beverage companies pivoting into the space. Increased competition could lead to margin compression, forcing PKP to lower its manufacturing fees to retain clients.

PKP is currently attempting to expand its operations into the USA (Florida facility). Executing a cross-border expansion in a complex regulatory environment carries significant operational execution risk. There is no guarantee that PKP can replicate its Canadian manufacturing success, secure the necessary state-level licenses, or attract enough US-based brands to make the new facility profitable.

Consumer adoption of THC beverages is still in its infancy. The entire investment thesis relies on the assumption that THC drinks will continue to take market share away from traditional alcohol. If consumer preferences shift, or if the initial novelty wears off and repeat purchase rates fall, the overall Total Addressable Market (TAM) for PKP’s services may be much smaller than anticipated.

Finally, PKP’s valuation is closely tied to sentiment in the broader cannabis and psychedelics sectors. These sectors are known for extreme volatility, often driven by political headlines rather than underlying company fundamentals. A negative shift in investor sentiment toward the sector could weigh heavily on PKP’s share price, regardless of its operational performance in Canada.

Investors should consider these risks carefully and seek professional advice tailored to their personal circumstances before investing.

Our PKP Investment Memo

Our Investment Memo provides a short, high-level summary of our reasons for Investing. We use this memo to track the progress of all our Investments over time.

In our PKP Investment Memo, you can find the following:

- What does PKP do?

- The macro theme for PKP

- Our PKP Big Bet

- What we want to see PKP achieve

- Why we are Invested in PKP

- The key risks to our Investment Thesis

- Our Investment Plan